We first began moving clients from Nucleus to Transact late 2021. This quarterly review shows our performance versus our industry peer group across our portfolios for a little over a 3 year period. 13 quarters so far.

In all of the charts below, each of our managed portfolios are shown by the bold green line. Our peers performance is shown in blue and purple lines.

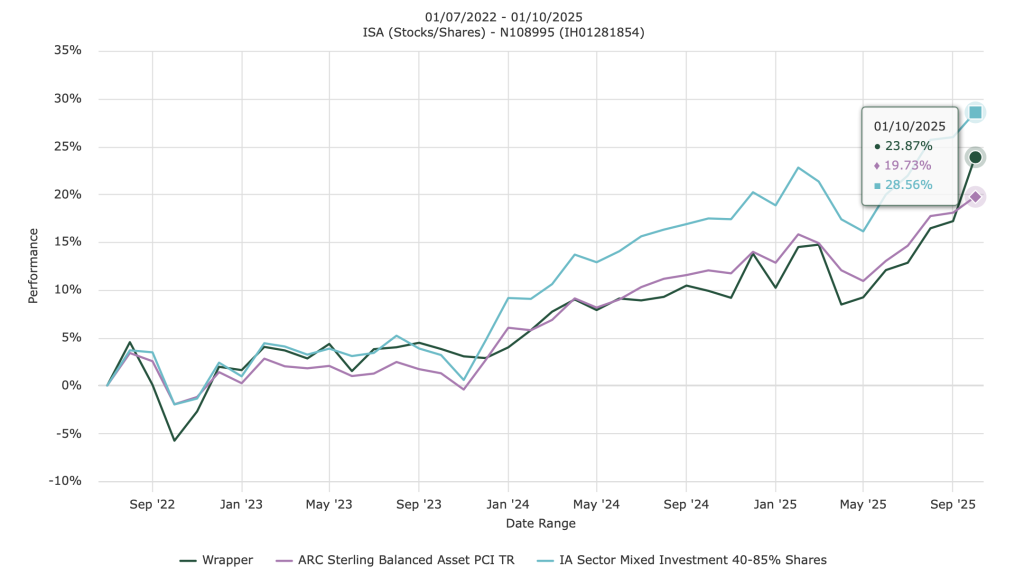

Our Cautious Portfolio

Our Cautious Managed Portfolio unfortunately is not a fair comparison versus its peer group as care home fees of several thousand pounds are withdrawn each month for the client in question. This reducing balance has blunted the true performance somewhat.

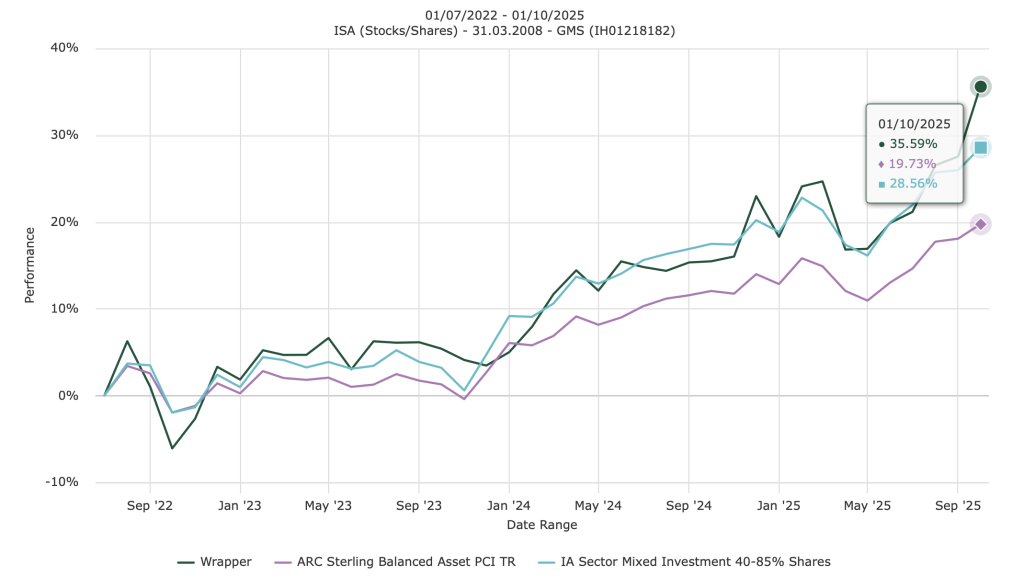

Our Moderate Portfolio

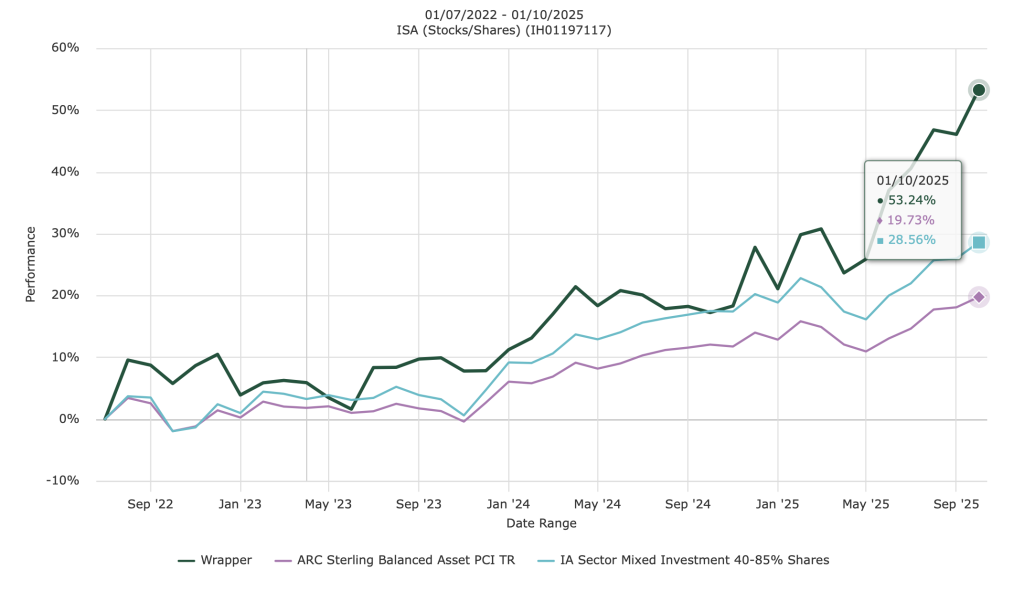

Our Aggressive Portfolio

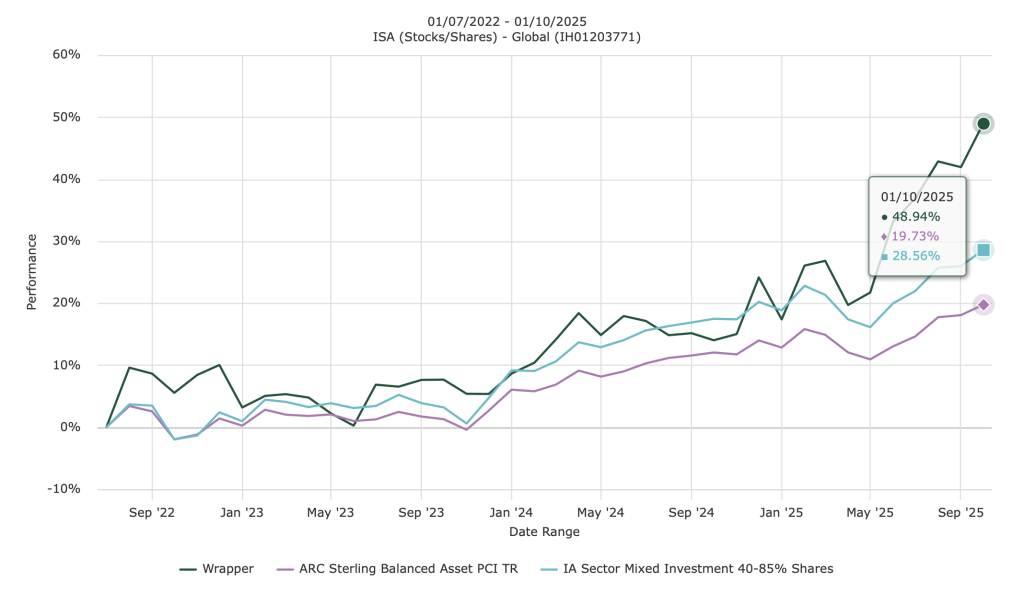

Our Very Aggressive Portfolio

Each of the charts above are actual client portfolios.

Our Very Aggressive Portfolio lost a little ground versus our Aggressive Portfolio whilst we exited some speculative positions before we could buy some precious metals and miners.

Commentary

We continue to out-perform our peer groups in all portfolios.

Continue reading “September 2025 Performance review”