Last time I wrote about how the bulk of our returns come through the winter months, the “Santa Rally” and of the first week in January dictating the direction of travel over the month, the quarter and indeed the year. I didn’t mention February.

A Typical February

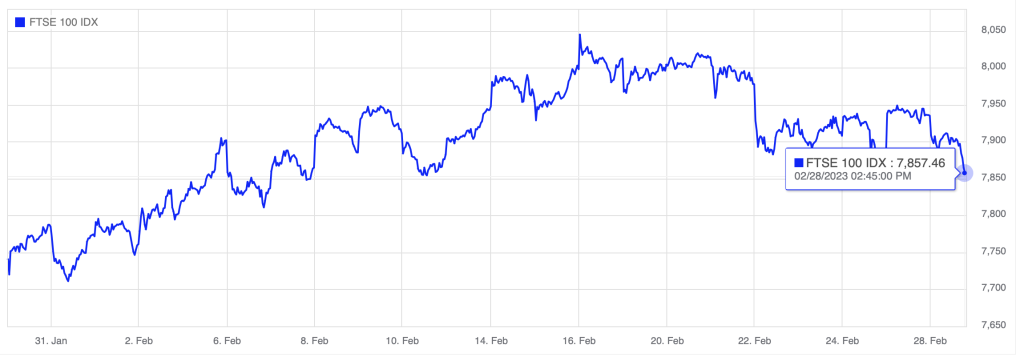

February started well but tailed off towards the end. Should we take it that the Fairy Tale recovery we are all waiting for has disappeared? Well no. February can usually be seen as a holding month, often a consolidation month after a strong start. On average, February is often a poor month within the 1st quarter performance in total.

The economic news did worsen this month though, but it hardly pointed to recession just yet.

Good News is Bad News!

As always, we look to the US and a much followed economic indicator. The payrolls report is a lagging indicator, as it quantifies what has happened, rather than what comes next. In the UK we concentrate on unemployment numbers, rather than the number of individuals in work.

First the good news: A strong January US jobs report showed better than expected levels of employment which is always good for an economy. 517,000 more people in jobs, a full 187,000 more than expected, which should translate to more consumers and growing, rather than contracting company valuations. US unemployment hits a 53 year low, the lowest it has been since May 1969 when The US were fighting communists in Vietnam!

Now the bad news: More consumers can lead to more demand for goods and services. A greater demand can lead to a shortage of supply, which leads to higher prices. The dreaded Inflation is set to continue despite the interest rate rises brought in by the FED to try to curb demand. The overall jobs market is certainly not showing any signs of stress, despite the number of construction jobs falling as new house builds are delayed due to high mortgage rates.

Economists suggested this report will lead to a likely further increase in interest rates, beyond what was previously expected. Market participants responded by driving up yields in the fixed interest markets by a further 0.75% compared with the expectation in January. Rising bond yields always dampen stock market valuations. Shares duly came down somewhat, leading to the worst week on Wall Street for 6 months.

All indicators are estimates and are often revised when the following months report is published. We will need to see just how close this estimate was. Let’s hope the February totals don’t over-shoot too.

The FTSE100 hit an all time high 8000 points!

As I write the level of the index had dropped back and today it is approaching 7850. I have described the FTSE100 in detail many times and it would be useful here if you could re-read a previous blog. Go on, it’s useful, I will wait for you to return.

https://hjscott.co.uk/things-you-maybe-didnt-know-about-uk-shares/

Welcome Back

The FTSE 100 Index, which is now comprised of just 100 shares is worth just over £2 trillion in total. That total is less than just the value of Apple, which explains why I am forever looking to see what the direction is in the US. The main UK index is weighted. That means the biggest companies are responsible for the bulk of the direction, whilst the smaller companies hardly move the dial. The top 11 companies now make up as much value as the next 89 companies when they are added together. Just the top 4 companies are 25% of the index in total.

So what happened to the top 4 to bring the index up to all time highs?

The re-opening of China happened. Shell, Astra Zeneca, HSBC & Unilever, all listed on the London Stock Exchange with a combined value of £578 billion making up a quarter of the index, all to some extent benefitted from the end of the Zero Covid policy of the Chinese Communist Party.

HSBC

Shares in Hong Kong & Shanghai Banking Corporation have added 46% in value since their recent October lows. The current value of HSBC shares, which halved since the advent of Covid hitting China, still sit well below their 2007 Great Financial Crisis highs. So for a decade and a half there has still not been a full recovery in value, but recently they have been running hot. Still I wouldn’t like to hold them if China invaded Taiwan.

Shell

Shell, the largest share of the UK index saw, the world’s largest consumer of oil re-open for business. The thinking is that even with oil prices dropping considerably from their Russian invasion highs, China will become very profitable, driving oil prices up once again in the same way prices in the West jumped once the Covid lockdowns ceased. The shares are up a more modest 12% over the period. The worry for investors here is a potential UK windfall tax on energy producers which could wreck the current share value.

Astra Zeneca

Astra Zeneca, the second largest share by value in the FTSE 100 does good business in China. Its Covid 19 vaccine is used extensively there. The market is so important that the global R&D unit is based in Shanghai. The recent fraud investigation which included falsifying patient notes and over charging medical insurance companies has not stopped the share rising in value by over 15% since October.

Unilever

Unilever sells 40 products to 150 million households in China. It operates an R&D centre there and dozens of world class factories. It sees China as its main engine of growth. It all started in Bolton when William Lever joined his parents grocery store around 1866. We have invested in Unilever in the past and maybe will again.

With the top 4 all hitting their stride at the same time, it mattered little what the rest of the more domestically orientated index toddlers achieved. By comparison the smallest share in the FTSE 100 index is Frasers, originally Mike Ashley Sports. With a market capitalisation of just £3.8 billion, it didn’t matter that it saw a rise in value over the period of 29% because it forms just 0.0018% of the index.

Welcome to March

Most portfolios ended February only slightly higher than they started despite the strong start to the month. For a February, it is indeed par for the course. March is usually strong, so fingers remain crossed for a strong end to the tax year. Look out for the end of March where a high quantity of options need to be settled. It usually gives a nice late uplift.

Last Orders

This month we will be moving funds between accounts to ensure that individuals ISA allowances have been used in full. We do this where a client has both a General Account and an ISA account on the same platform. Hands up if you would like to pay more in tax than you need to? Thought not.

If you would like to add directly to your ISAs, or indeed any of your accounts whilst the market takes this temporary pause, please get in touch

It’s also the month to maximise on tax relief for those higher rate tax-payers amongst us. Please don’t leave it to the last minute as appointments fill up thick and fast. Call us now to get that review booked.

Very informative blog Howard, much appreciated.

I have a question for you. Could the Chancellor be considering capping ISA holdings in the future in his quest to squeeze out more tax from those who can afford it?

Hi Peter

As always no stone is left unturned when it comes to raising tax to fund this country’s horrendous deficit. I have read it is a consideration. Logistically it is difficult because every ISA holding would require an income and capital gains tax calculation performing, then an allowance would be made up to the cap. A more likely and much easier move would be to restrict further contributions in to ISAs for those above a certain limit already. Very unpopular I would have thought with core Conservative voters and perhaps an own goal as corporation tax from investment management companies could be drastically reduced.